Mastercard

Founded Year

1966Stage

IPO | IPODate of IPO

5/25/2006Market Cap

488.57BStock Price

544.07Revenue

$0000About Mastercard

Mastercard operates as a global company focused on digital payment processing and financial technology services. The company provides digital payment solutions that ensure transactions are secure and accessible. Mastercard's products and services cater to individuals, businesses, and governments. Mastercard was formerly known as Master Charge. It was founded in 1966 and is based in Purchase, New York.

Loading...

ESPs containing Mastercard

The ESP matrix leverages data and analyst insight to identify and rank leading companies in a given technology landscape.

The card-linked rewards programs market enables financial institutions, merchants, and loyalty program operators to automatically apply rewards when consumers make purchases with linked payment cards. These platforms eliminate friction by removing the need for manual coupon activation or loyalty card presentation at point-of-sale. Key capabilities include real-time transaction monitoring, personal…

Mastercard named as Leader among 15 other companies, including Visa, American Express, and Citibank.

Loading...

Research containing Mastercard

Get data-driven expert analysis from the CB Insights Intelligence Unit.

CB Insights Intelligence Analysts have mentioned Mastercard in 23 CB Insights research briefs, most recently on Oct 23, 2025.

Oct 23, 2025 report

Fintech 100: The most promising fintech startups of 2025

Oct 3, 2025 report

Dual AI engines: LLMs and optimizers sweep September mega-round funding

Sep 23, 2025 report

The Money Awards Finalist Spotlight

Sep 12, 2025

How payments leaders are seizing the SMB opportunity

Aug 22, 2025

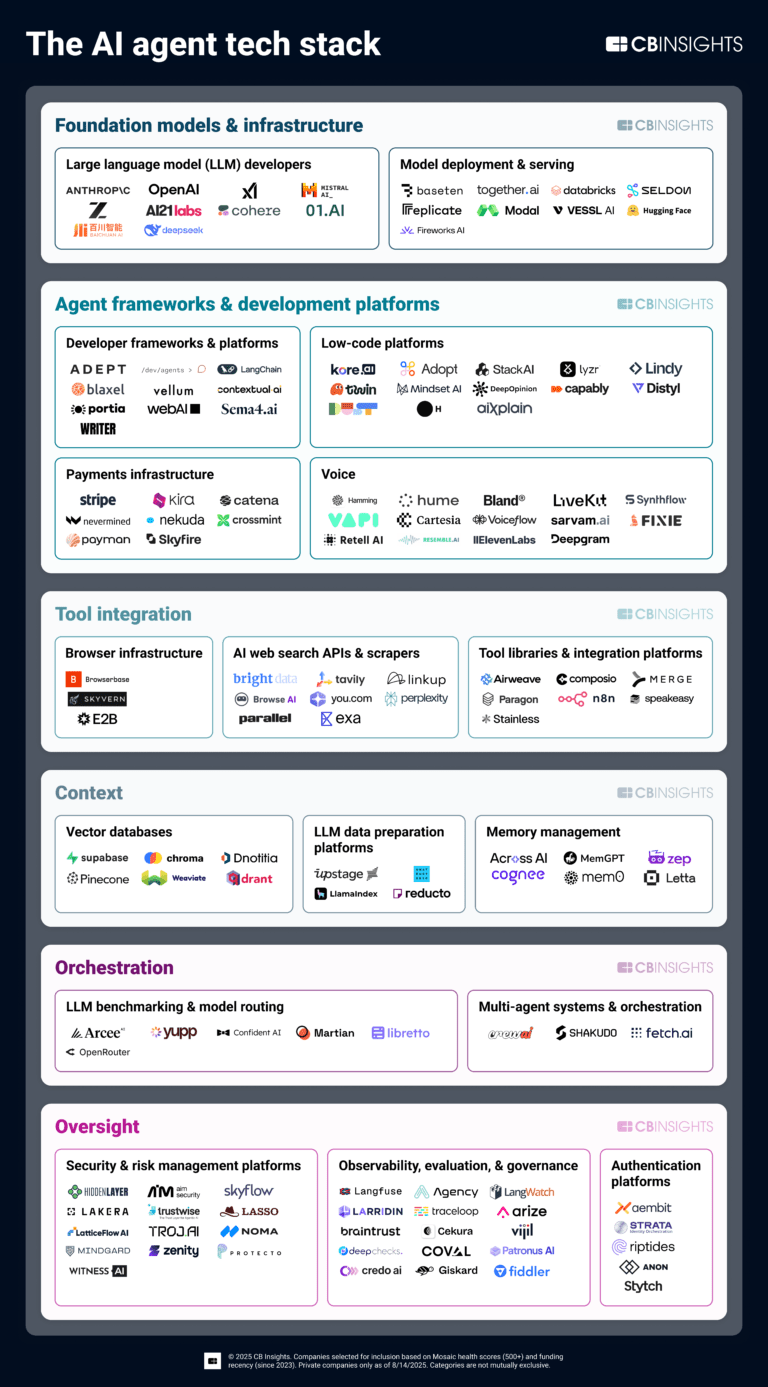

The AI agent tech stack

Aug 7, 2025

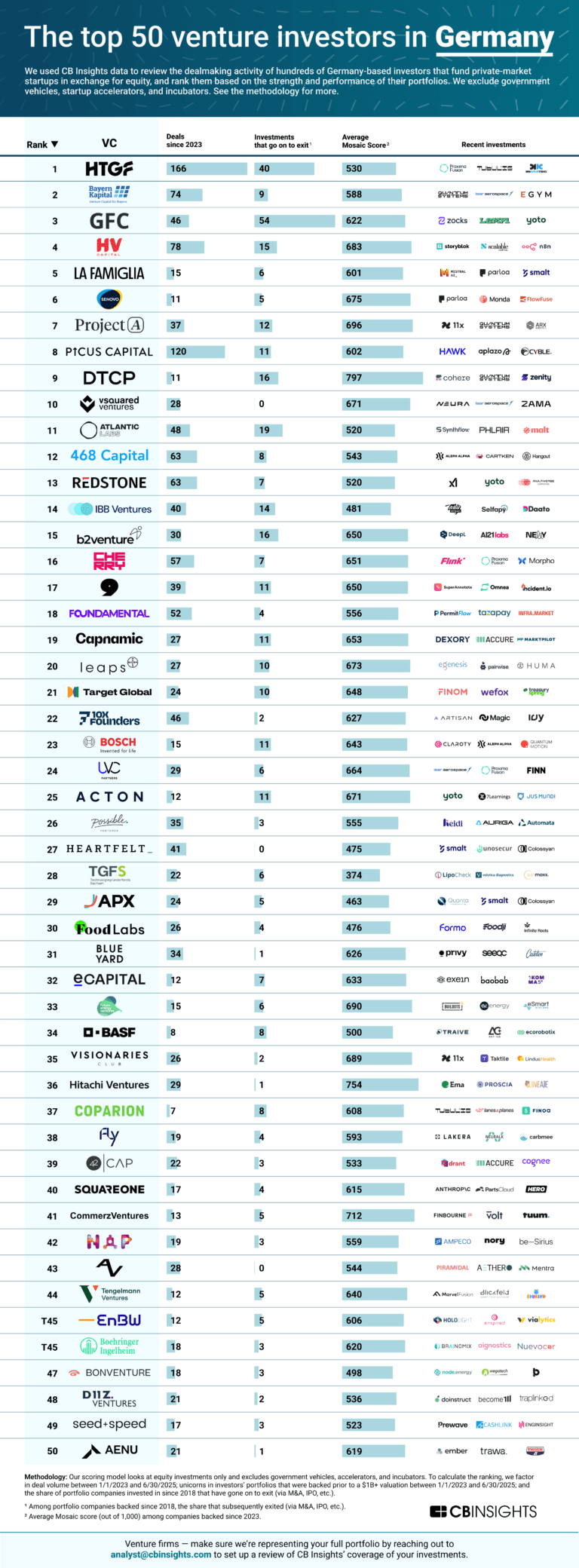

The top 50 venture investors in Germany

Aug 4, 2025

3 markets fueling the shift to agentic commerceExpert Collections containing Mastercard

Expert Collections are analyst-curated lists that highlight the companies you need to know in the most important technology spaces.

Mastercard is included in 9 Expert Collections, including Blockchain.

Blockchain

9,320 items

Companies in this collection build, apply, and analyze blockchain and cryptocurrency technologies for business or consumer use cases. Categories include blockchain infrastructure and development, crypto & DeFi, Web3, NFTs, gaming, supply chain, enterprise blockchain, and more.

Gig Economy Value Chain

155 items

Startups in this collection are leveraging technology to provide financial services and HR offerings to the gig economy industry

Conference Exhibitors

5,302 items

Fintech

9,809 items

Companies and startups in this collection provide technology to streamline, improve, and transform financial services, products, and operations for individuals and businesses.

Digital Banking

108 items

Silicon Valley Bank's Fintech Network

88 items

We mapped out some of SVB's biggest clients, partnerships, and sectors that it serves using CB Insights’ business relationship data from SVB’s profile to uncover just how important it is to the fintech universe. The list is not exhaustive.

Mastercard Patents

Mastercard has filed 4329 patents.

The 3 most popular patent topics include:

- payment systems

- credit cards

- payment service providers

Application Date | Grant Date | Title | Related Topics | Status |

|---|---|---|---|---|

9/27/2021 | 4/8/2025 | Data modeling, Software engineering researchers, Data management, Database researchers, Parallel computing | Grant |

Application Date | 9/27/2021 |

|---|---|

Grant Date | 4/8/2025 |

Title | |

Related Topics | Data modeling, Software engineering researchers, Data management, Database researchers, Parallel computing |

Status | Grant |

Latest Mastercard News

Nov 4, 2025

As of November 2025, stablecoins are shedding their image as mere crypto trading tools, evolving into a foundational infrastructure for a more efficient, inclusive, and integrated global financial system. Recent innovations, including yield-bearing stablecoins, enhanced programmability, and real-world asset (RWA) backing, are dramatically expanding their utility for payments, remittances, and institutional finance. This technological evolution is being met with a wave of comprehensive regulatory frameworks worldwide, most notably the European Union's Markets in Crypto-Assets (MiCA) regulation, which became fully applicable for Crypto-Asset Service Providers (CASPs) on December 30, 2024, and the United States' Guiding and Establishing National Innovation for US Stablecoins (GENIUS) Act, signed into law on July 18, 2025. These regulatory milestones, alongside efforts in the UK, Japan, Singapore, and Hong Kong, are instilling unprecedented trust and stability by mandating robust reserve requirements, transparency, and consumer protection. The combined effect is a powerful catalyst for broader adoption, positioning stablecoins as a critical bridge between traditional finance and the burgeoning digital economy. Market Impact and Price Action While stablecoins are inherently designed to maintain a stable peg to fiat currencies, the recent technological and regulatory advancements have had a profound impact on the broader crypto market's structure, liquidity, and risk profile. The increased regulatory clarity, particularly from MiCA and the GENIUS Act, has significantly de-risked the stablecoin sector, leading to a noticeable shift in institutional perception and engagement. This newfound confidence has translated into enhanced liquidity depth across major stablecoin pairs, making large-volume transactions more efficient and less prone to slippage. The market has responded positively to the elimination of risky algorithmic stablecoin models, with MiCA explicitly banning them within the EU and the GENIUS Act focusing on fully reserved, high-quality asset-backed stablecoins in the US. This has mitigated systemic risks that previously plagued the market, as evidenced by past events such as the Terra/LUNA collapse. The market is now witnessing a preference for regulated, transparently backed stablecoins, which are increasingly being integrated into traditional financial workflows. Furthermore, the emergence of yield-bearing stablecoins, backed by real-world assets like U.S. Treasuries, is creating a new paradigm for capital efficiency within the crypto ecosystem. These innovations offer investors the ability to earn passive income on stable digital assets without exposure to crypto volatility, effectively attracting capital that might otherwise remain in traditional finance. This trend is fostering deeper integration between DeFi and TradFi, expanding the total addressable market for stablecoin-based financial products and services. The increased utility and trust are driving higher stablecoin transaction volumes, often surpassing traditional payment networks, thereby solidifying their role as essential market infrastructure. Community and Ecosystem Response The crypto community, developers, and traditional financial institutions have reacted with a mix of enthusiasm and strategic recalibration to the stablecoin revolution. Social media sentiment reflects a growing appreciation for regulatory clarity, with many users viewing frameworks like MiCA and the GENIUS Act as crucial steps toward mainstream adoption and investor protection. Crypto influencers and thought leaders widely acknowledge that robust regulation is a necessary evil, paving the way for institutional capital and broader public trust. Developers are actively leveraging the enhanced programmability of stablecoins to build more sophisticated DeFi protocols and Web3 applications. The ability to create automated, rules-based transactions through smart contracts is unlocking new business models, including usage-based pricing, streaming payments, and integrated compliance checks. Major financial institutions, including JPMorgan ( NYSE: JPM ), Citi ( NYSE: C ), Western Union ( NYSE: WU ), Visa ( NYSE: V ), and Mastercard ( NYSE: MA ), are increasingly integrating stablecoins into their operations for digital asset payments, tokenized treasuries, and on-chain financing. This signifies a strong institutional endorsement, transforming stablecoins into essential tools for corporate finance and treasury management, offering unprecedented speed and predictability. The broader crypto Twitter and Reddit communities are buzzing with discussions about the implications of yield-bearing stablecoins and tokenized deposits for financial inclusion and capital efficiency. While some purists express concerns about potential centralization under strict regulatory regimes, the prevailing sentiment is that the benefits of enhanced stability, consumer protection, and institutional integration outweigh these concerns, especially for fostering long-term growth and legitimacy of the crypto ecosystem. What's Next for Crypto The trajectory for stablecoins in the short to long term is one of continued integration and expansion, with significant implications for the entire crypto market. In the short term, the focus will be on the practical implementation of new regulatory frameworks. Regulators, particularly in the U.S., are now tasked with writing detailed rules for the GENIUS Act, which will further shape the operational landscape for stablecoin issuers. This period will likely see existing stablecoin providers adapt their structures and offerings to comply with these new mandates, potentially leading to a consolidation of the market around well-regulated entities. Long-term implications point towards stablecoins becoming the primary on-ramp and off-ramp for digital assets, facilitating seamless interaction between traditional finance and the decentralized world. Potential catalysts include further advancements in blockchain interoperability and Layer 2 solutions, which will continue to enhance the scalability and efficiency of stablecoin transactions, making them even more attractive for high-volume, low-cost global payments. The ongoing development of payment orchestration layers will also simplify user experience, abstracting away blockchain complexities and making stablecoin usage as straightforward as traditional bank transfers. Strategic considerations for projects and investors involve prioritizing stablecoins issued by compliant entities with transparent, high-quality reserves. Projects building in DeFi or Web3 should integrate with these regulated stablecoins to ensure future compatibility and access to institutional liquidity. Investors should monitor regulatory updates closely, as shifts in policy could impact the viability and structure of certain stablecoin models. Possible scenarios include a future where central bank digital currencies (CBDCs) coexist with highly regulated private stablecoins, each serving distinct but complementary roles in a multi-layered digital financial system. The likelihood of this integrated future is high, driven by the clear benefits of efficiency and programmability. Bottom Line For crypto investors and enthusiasts, the key takeaway is that stablecoins are no longer just a safe haven during market volatility; they are evolving into a fundamental building block of the future financial system. The twin forces of technological innovation and comprehensive global regulation are making stablecoins more versatile, reliable, and secure than ever before. Investors should prioritize stablecoins that adhere to stringent regulatory standards, such as those compliant with MiCA in the EU or the GENIUS Act in the US, as these offer greater assurance of peg stability and consumer protection. The long-term significance of these developments cannot be overstated. Stablecoins are poised to drive crypto adoption by providing a stable, efficient, and increasingly regulated medium for global payments, remittances, and institutional finance. They bridge the gap between volatile cryptocurrencies and the stability of fiat currencies, unlocking new possibilities for financial inclusion and capital efficiency. The ongoing institutional integration, evidenced by the involvement of major players like JPMorgan ( NYSE: JPM ) and Visa ( NYSE: V ), signals a maturation of the digital asset space and a clear path towards widespread acceptance. Important dates and metrics to monitor include the full implementation timelines for MiCA and the GENIUS Act, particularly the release of detailed rules by US regulators. Investors should also watch for increasing transaction volumes of regulated stablecoins, the growth of yield-bearing stablecoin offerings, and further partnerships between traditional financial institutions and stablecoin issuers. These indicators will collectively paint a picture of stablecoins' continued ascent as a cornerstone of the global digital economy. This article is for informational purposes only and does not constitute financial or investment advice. Cryptocurrency investments carry significant risk.

Mastercard Frequently Asked Questions (FAQ)

When was Mastercard founded?

Mastercard was founded in 1966.

Where is Mastercard's headquarters?

Mastercard's headquarters is located at 2000 Purchase Street, Purchase.

What is Mastercard's latest funding round?

Mastercard's latest funding round is IPO.

Who are Mastercard's competitors?

Competitors of Mastercard include Klarna, Payall, Discover, Worldpay, Revolut and 7 more.

Loading...

Compare Mastercard to Competitors

Ant Group focuses on digital transformation infrastructure and platform development for the service industry. The company aims to provide equal access to financial and other services that are inclusive, green, and sustainable for consumers and small businesses. Ant Group was formerly known as Zhejiang Ant Micro Financial Service Group. It was founded in 2004 and is based in Hangzhou, China.

InComm Payments is a provider of payment technology solutions across various industries. The company specializes in cash digitization, card solutions, account funding, and payment services, including healthcare benefits, gifting, and incentives. InComm Payments serves sectors such as retail, healthcare, and transit with its suite of payment products and services. It was founded in 1992 and is based in Atlanta, Georgia.

Interac operates as a financial technology company offering digital payment solutions and identity verification services. The company provides services such as Interac Debit for in-store payments, Interac e-Transfer for sending and receiving money online, and Interac Direct for online shopping payments. Interac also offers solutions for individuals and businesses to authenticate identities and transactions. Interac was formerly known as Acxsys. It was founded in 1984 and is based in Toronto, Canada.

PayPay operates as a financial technology company providing quick response (QR) code-based payment solutions and digital wallet services. The company offers a platform for users to make payments at various retail locations, online, and for public utilities, as well as facilitating peer-to-peer money transfers. PayPay primarily serves the consumer goods retail, dining, and public utility payment sectors. It was founded in 2018 and is based in Tokyo, Japan.

Moneris Solutions provides commerce solutions within the financial technology sector. The company offers services including payment processing, point-of-sale systems, and online payment gateways for businesses. Moneris Solutions serves the retail, restaurant, professional services, and public sector industries with commerce solutions. It was founded in 2000 and is based in Toronto, Canada.

Amazon Pay is a digital payment platform that offers financial services such as mobile recharges, bill payments, and purchases of digital gift cards and vouchers. It also facilitates payments for travel tickets and insurance premiums. It is based in India.

Loading...