Meta

Founded Year

2004Stage

PIPE - II | IPOTotal Raised

$2.509BMarket Cap

1634.18BStock Price

637.71Revenue

$0000About Meta

Meta operates as a technology company focused on building the future of human connection through social media and immersive experiences. The company provides services, including social networking platforms, instant messaging, and photo-sharing applications, as well as augmented and virtual reality services. It serves individual users and businesses aiming to connect and grow within digital communities. Meta was formerly known as Facebook. It was founded in 2004 and is based in Menlo Park, California.

Loading...

Loading...

Research containing Meta

Get data-driven expert analysis from the CB Insights Intelligence Unit.

CB Insights Intelligence Analysts have mentioned Meta in 53 CB Insights research briefs, most recently on Oct 30, 2025.

Oct 30, 2025 report

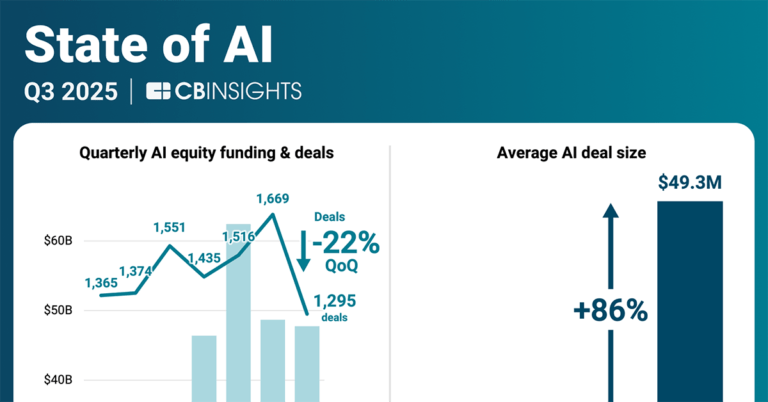

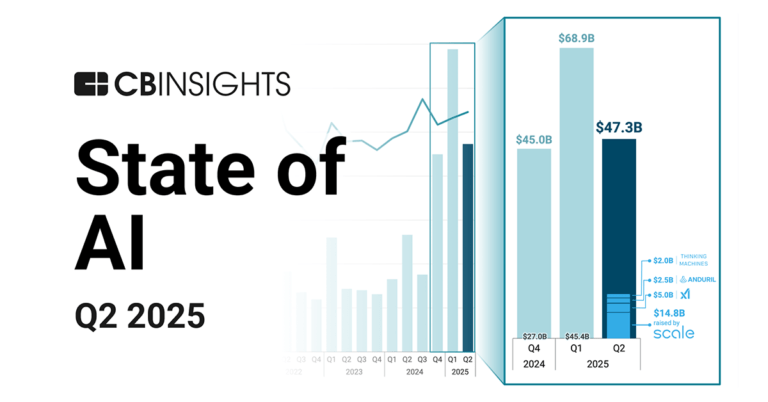

State of AI Q3’25 Report

Sep 11, 2025

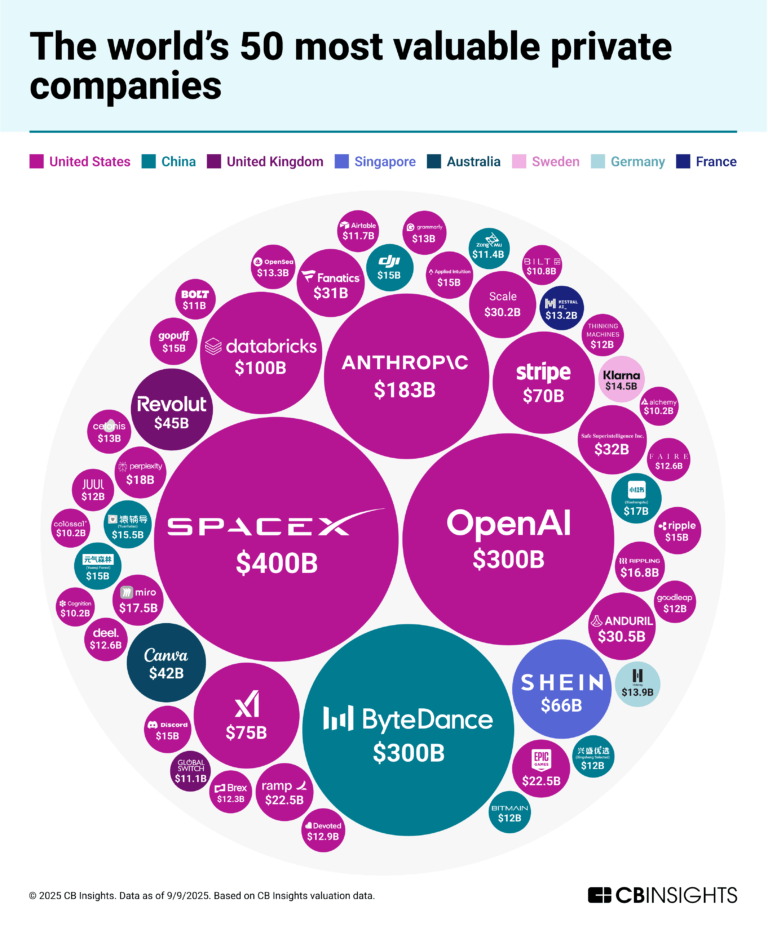

The world’s 50 most valuable private companies

Aug 22, 2025

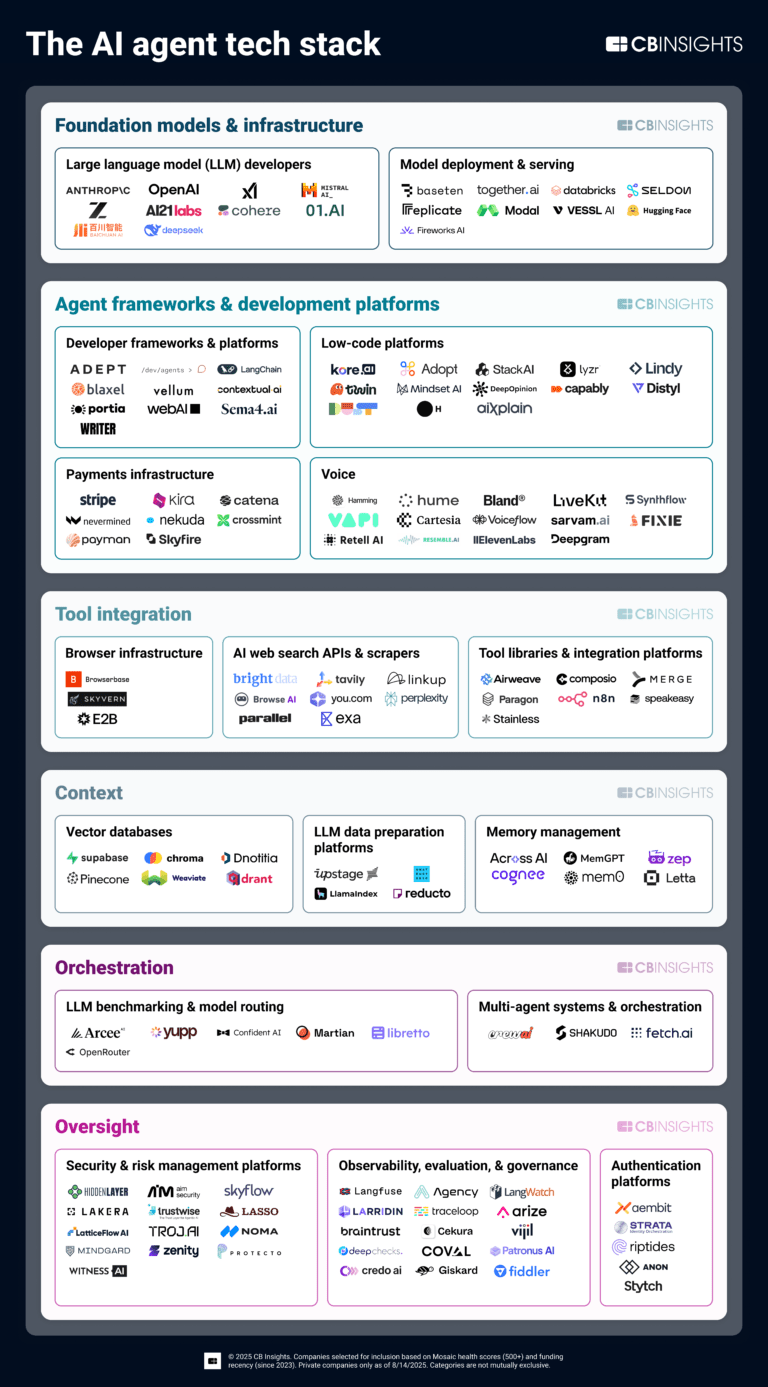

The AI agent tech stack

Jul 31, 2025 report

State of AI Q2’25 ReportExpert Collections containing Meta

Expert Collections are analyst-curated lists that highlight the companies you need to know in the most important technology spaces.

Meta is included in 3 Expert Collections, including Fortune 500 Investor list.

Fortune 500 Investor list

590 items

This is a collection of investors named in the 2019 Fortune 500 list of companies. All CB Insights profiles for active investment arms of a Fortune 500 company are included.

Grid and Utility

2,383 items

Companies that are developing and implementing new technologies to optimize the grid and utility sector. This includes, but is not limited to, distributed energy resources, infrastructure security, utility asset management, grid inspection, energy efficiency, grid storage, etc.

Conference Exhibitors

5,302 items

Meta Patents

Meta has filed 10000 patents.

The 3 most popular patent topics include:

- virtual reality

- mixed reality

- augmented reality

Application Date | Grant Date | Title | Related Topics | Status |

|---|---|---|---|---|

2/28/2021 | 4/8/2025 | Actuators, Valves, Automation, Raytheon products, Engine technology | Grant |

Application Date | 2/28/2021 |

|---|---|

Grant Date | 4/8/2025 |

Title | |

Related Topics | Actuators, Valves, Automation, Raytheon products, Engine technology |

Status | Grant |

Latest Meta News

Nov 4, 2025

This sharp ascent, driven by a hawkish Federal Reserve, persistent inflation concerns, and substantial government borrowing, is immediately bolstering the U.S. dollar while simultaneously exerting considerable downward pressure on the prices of gold and silver. As of November 3, 2025, this shift is reshaping investor sentiment and forcing a re-evaluation of market strategies, with profound implications for asset allocation and future economic outlooks. This surge in yields reflects a complex interplay of factors, signaling a recalibration of expectations regarding interest rates and economic growth. While the dollar enjoys a renewed appeal as a safe-haven and high-yield currency, precious metals, traditionally seen as inflation hedges and safe stores of value, are facing headwinds. The unfolding scenario highlights the sensitivity of global markets to U.S. monetary policy and fiscal health, setting the stage for a period of heightened volatility and strategic adjustments across various asset classes. Yields Climb Amidst Fed Hawkishness and Fiscal Pressures The recent climb in U.S. Treasury note yields is a direct consequence of several interconnected factors, creating a complex environment for investors. A pivotal driver has been the Federal Reserve's (Fed) increasingly hawkish stance, particularly following statements from Chair Jerome Powell. Despite a recent 25-basis-point rate cut, Powell's emphasis on persistent inflation and a resilient U.S. economy has led markets to significantly scale back expectations for further rate cuts in 2025. This unexpected hawkishness, with some Fed officials openly preferring to maintain current rates, caused a notable spike in yields, especially for the 2-year Treasury note, as the certainty of a December rate cut diminished. Compounding this monetary policy narrative is the ongoing government shutdown, which commenced on October 1. This shutdown has resulted in a critical data blackout, preventing the release of essential economic indicators like jobs numbers and inflation reports. This vacuum of information has amplified market uncertainty, making it challenging for both policymakers and investors to accurately gauge economic trends, thereby contributing to increased market volatility and upward pressure on yields. Furthermore, the U.S. Treasury's plan to borrow a substantial $569 billion this quarter, coupled with large bond offerings from major tech giants such as Meta Platforms ( NASDAQ: META ) and Alphabet ( NASDAQ: GOOGL ), is increasing the overall supply of debt. This significant issuance is diverting investor capital from government bonds, raising borrowing costs, and consequently pushing Treasury yields higher. Persistent concerns about inflation continue to underpin the Fed's "higher-for-longer" interest rate policy, providing sustained upward pressure on yields. The U.S. economy's unexpected resilience, evidenced by strong manufacturing data and robust overall performance, has also contributed to rising real yields. Moreover, anxieties surrounding the U.S. fiscal outlook, particularly with pre-election spending agendas that appear to lack a focus on deficit reduction, are raising concerns about escalating U.S. debt levels. These fiscal worries are contributing to a higher term premium in the bond market, further entrenching the upward trend in Treasury yields and reshaping the landscape for global finance. Corporate Fortunes Tied to Interest Rate Dynamics The surge in U.S. Treasury yields creates a distinct divide between potential winners and losers among public companies, primarily based on their balance sheet structure, debt exposure, and sector-specific sensitivities to interest rates. Potential Winners: Financial Institutions: Banks and other financial services companies, such as JPMorgan Chase ( NYSE: JPM ), Bank of America ( NYSE: BAC ), and Wells Fargo ( NYSE: WFC ), typically benefit from a rising interest rate environment. Higher yields often translate to improved net interest margins (NIM), as the interest they earn on loans and investments increases more rapidly than the interest they pay on deposits. This can lead to increased profitability and stronger earnings reports. Insurance companies also stand to gain as the returns on their investment portfolios, often heavily weighted in fixed-income securities, improve. Companies with Strong Cash Flows and Low Debt: Businesses with robust free cash flows and minimal reliance on debt financing are better positioned to weather a high-yield environment. They are less exposed to rising borrowing costs and can even capitalize on opportunities by acquiring distressed assets or investing in growth without incurring prohibitive debt expenses. Value Stocks: In a rising rate environment, investors often rotate out of growth stocks, which are valued on future earnings, and into value stocks, which tend to have more immediate earnings and often pay dividends. Sectors like utilities and certain consumer staples might see renewed interest. Potential Losers: Growth and Technology Companies: High-growth technology companies, particularly those that rely heavily on future earnings projections to justify their valuations and often require significant capital for expansion, are vulnerable. Companies like Tesla ( NASDAQ: TSLA ), Nvidia ( NASDAQ: NVDA ), or even the aforementioned Meta Platforms ( NASDAQ: META ) and Alphabet ( NASDAQ: GOOGL ) (despite their size and strong cash flows, their bond offerings indicate borrowing needs) can see their borrowing costs increase significantly, impacting profitability and slowing investment. The discounted value of their future earnings also decreases when discount rates (tied to yields) rise, making their stocks less attractive. Highly Leveraged Companies: Companies with substantial outstanding debt, especially those with variable-rate loans or significant refinancing needs, will face higher interest expenses. This can erode profit margins, strain cash flow, and potentially lead to financial distress. Sectors such as real estate, utilities with heavy infrastructure investments, and certain industrials might be particularly exposed. Commodity Producers (Gold and Silver Miners): While the underlying commodities (gold and silver) are pressured by rising yields, the mining companies themselves, such as Barrick Gold ( NYSE: GOLD ) or Wheaton Precious Metals ( NYSE: WPM ), can face a double whammy. Not only do their revenue streams potentially shrink due to lower commodity prices, but their operational costs and capital expenditures, often financed through debt, become more expensive. This can squeeze profit margins and impact their ability to fund new projects or maintain existing operations. The current environment demands careful financial management and strategic planning from companies across the board, with those boasting strong balance sheets and adaptable business models best positioned to navigate the challenges and potentially capitalize on the opportunities presented by elevated Treasury yields. Broader Implications and Historical Parallels The surge in U.S. Treasury yields extends far beyond immediate market reactions, carrying significant broader implications for the global financial landscape. This event fits into a larger trend of developed economies grappling with persistent inflation, robust labor markets, and the winding down of ultra-loose monetary policies. The Federal Reserve's commitment to a "higher-for-longer" interest rate stance, even amidst a recent rate cut, signals a fundamental shift from the low-interest-rate environment that characterized much of the post-2008 era. This paradigm shift affects everything from consumer borrowing costs to international capital flows. The ripple effects are profound. For emerging markets, a stronger U.S. dollar and higher U.S. yields can lead to capital outflows, making it more expensive for these nations to service dollar-denominated debt and potentially destabilizing their currencies and economies. Competitors and partners of U.S. companies also face increased pressure. For instance, European and Asian exporters might find their goods more expensive for U.S. buyers due to the stronger dollar, impacting trade balances. Regulatory bodies, particularly central banks globally, will be closely watching the Fed's actions, as their own monetary policy decisions are often influenced by U.S. interest rate differentials. The ongoing government shutdown further complicates the picture, creating a data vacuum that hinders accurate economic assessment and potentially forces a more cautious approach from regulators. Historically, periods of rising U.S. Treasury yields have often coincided with periods of economic strength or inflationary pressures. For example, the early 1980s saw significant yield increases as the Fed, under Paul Volcker, aggressively combated inflation. While the current context differs, particularly with global supply chain complexities and geopolitical tensions, the principle remains: higher yields reflect either robust economic activity (leading to higher demand for capital) or increased inflation expectations (demanding higher compensation for lenders), or a combination of both. Comparing this to similar events, such as the "taper tantrum" of 2013, highlights the market's sensitivity to central bank communication and the potential for rapid adjustments when policy expectations shift. The key difference now is the added layer of fiscal uncertainty and the sheer scale of government borrowing, which adds a structural component to the yield pressure. This environment underscores a broader move towards fiscal prudence and market discipline, as governments face increasing scrutiny over their debt trajectories. The Path Ahead: Navigating a High-Yield Environment Looking ahead, the trajectory of U.S. Treasury yields will be a dominant factor shaping market dynamics in the short and long term. In the immediate future, market participants will be intensely focused on any signals from the Federal Reserve regarding its monetary policy path. The ongoing government shutdown and the subsequent data blackout mean that upcoming economic data releases, once available, will be scrutinized for clarity on inflation and employment. Any signs of cooling inflation or a weakening labor market could temper the "higher-for-longer" narrative, potentially providing some relief to yields. Conversely, persistent inflation and a resilient economy would reinforce the current trend, pushing yields even higher. For companies and investors, strategic pivots and adaptations will be crucial. Businesses with significant debt loads will need to prioritize debt reduction or explore refinancing options to mitigate rising interest expenses. Sectors like real estate, which are highly sensitive to borrowing costs, may experience a slowdown in investment and development. Conversely, opportunities may emerge for financial institutions to expand their lending margins and for value-oriented investors to find attractive entry points in sectors that benefit from higher rates. The strengthening dollar, while challenging for some exporters, could offer advantages for importers and U.S. consumers through cheaper foreign goods. Potential scenarios range from a continued gradual ascent in yields, driven by sustained economic growth and inflation, to a more volatile period marked by rapid fluctuations based on incoming data and Fed commentary. A "soft landing" scenario, where inflation recedes without a significant economic downturn, might see yields stabilize at elevated levels. However, a "hard landing" or recession could lead to a sharp reversal in yields as investors flock back to safe-haven Treasuries. The long-term outlook will also depend on the U.S. fiscal situation; if government borrowing continues unchecked, structural pressure on yields will persist, regardless of short-term economic fluctuations. Investors should prepare for a landscape where capital is more expensive, and the relative attractiveness of different asset classes is constantly being re-evaluated based on the evolving interest rate environment. Market Recalibration and Enduring Impact The recent surge in U.S. Treasury note yields represents a significant recalibration of financial markets, moving away from an era of ultra-low interest rates towards a more normalized, albeit elevated, cost of capital. The key takeaways from this event are multi-faceted: the Federal Reserve's hawkish stance is firmly in place, prioritizing inflation control even at the expense of growth; the U.S. dollar is reasserting its strength as higher yields attract global capital; and precious metals like gold and silver are facing structural headwinds from a stronger dollar and increased opportunity cost, despite some underlying support from industrial demand and central bank buying. Moving forward, the market will remain highly sensitive to monetary policy signals, inflation data, and the U.S. fiscal trajectory. Investors should expect continued volatility as these factors play out. The "higher-for-longer" interest rate paradigm is likely to persist, influencing corporate profitability, consumer spending, and international capital flows. This environment will favor companies with strong balance sheets, robust cash flows, and those operating in sectors that benefit from or are resilient to higher borrowing costs. The lasting impact of this yield surge could be a fundamental shift in investment strategies, with a greater emphasis on value, dividend-paying stocks, and less speculative assets. The era of cheap money that fueled rapid growth in certain sectors may be drawing to a close, ushering in a period where capital allocation decisions are made with greater scrutiny on returns and risk. What investors should watch for in the coming months includes the resolution of the government shutdown and the subsequent release of crucial economic data, any shifts in the Federal Reserve's rhetoric, and the market's reaction to corporate earnings reports under the new interest rate regime. The interplay of these elements will determine the extent and duration of this market recalibration and its ultimate legacy on the financial landscape. This content is intended for informational purposes only and is not financial advice

Meta Frequently Asked Questions (FAQ)

When was Meta founded?

Meta was founded in 2004.

Where is Meta's headquarters?

Meta's headquarters is located at 1 Hacker Way, Menlo Park.

What is Meta's latest funding round?

Meta's latest funding round is PIPE - II.

How much did Meta raise?

Meta raised a total of $2.509B.

Who are the investors of Meta?

Investors of Meta include PIF, Firsthand Technology Value Fund, Tri-Pillar Investments, T. Rowe Price, Kleiner Perkins and 33 more.

Who are Meta's competitors?

Competitors of Meta include X, Reddit, ByteDance, Discord, AppLovin and 7 more.

Loading...

Compare Meta to Competitors

Oath operates within the media and technology sectors. The company offers services that include media content delivery and advertising solutions for advertisers and publishers. These services aim to facilitate interactions between brands and consumers, as well as assist publishers in business growth. Oath was formerly known as AOL Advertising. It was founded in 2017 and is based in Sterling, Virginia.

ByteDance provides content platforms in the social media and entertainment sectors. It offers products that enable content creation, discovery, and sharing, including short-form video platforms, social media services, and enterprise collaboration tools. Its products serve a global audience. It was formerly known as Beijing ByteDance Technology Co. It was founded in 2012 and is based in Beijing, China.

Bluesky is a social media platform with a goal of establishing an open foundation for the social internet. It provides a space for users to interact with content and utilize tools for moderation and customization. The company operates within the social media industry and aims to support a developer ecosystem. It was founded in 2021 and is based in Seattle, Washington.

Ditto specializes in communication tools within the social media and messaging domain. It provides technology that enables users to interact with their friends' bots, chat, play games, and share stories while offline. The company's target customers include individuals who use social media and digital communication. It was founded in 2023 and is based in Devon, United Kingdom.

Mozilla is a notforprofit organization that focuses on internet browser technology and user privacy protection. The company offers a suite of products, including the Firefox browser, a virtual private network service, and tools for password management and data breach monitoring. Mozilla primarily serves individual internet users and web developers. It was founded in 1998 and is based in San Francisco, California.

NextRoll focuses on machine learning and data insights. The company provides two platforms: RollWorks for account-based marketing and sales teams, and AdRoll for e-commerce marketing targeting direct-to-consumer brands. Its technology stack enables businesses to target and engage their audiences effectively. NextRoll was formerly known as Semantic Sugar. It was founded in 2006 and is based in San Francisco, California.

Loading...